How to Read a Cheque: A Complete Step-by-Step Guide

Understanding Your Paper Turnover

Even in our digital banking era, knowing how to read a cheque remains an essential financial literacy skill. Whether you are setting up a direct deposit, writing a payment for rent, or verifying a business transaction, paper cheques still anchor major parts of the financial system. According to compliance and operational guidelines set by central authorities like the Federal Reserve System, standardizing these paper documents ensures that billions of dollars move securely between accounts every day.

Understanding the layout of a cheque prevents costly financial errors. Misreading a digit or misidentifying a number can delay payments, cause overdraft fees, or disrupt your payroll. This comprehensive guide explains every element on a cheque, what the numbers mean, and how to use them with confidence. If you’re looking to strengthen your overall financial knowledge, don’t miss our guide on credit card tips you need to know. Taking a few minutes to master the layout of a cheque protects your hard-earned money and makes everyday banking tasks much easier.

The Anatomy of a Cheque: Front Layout

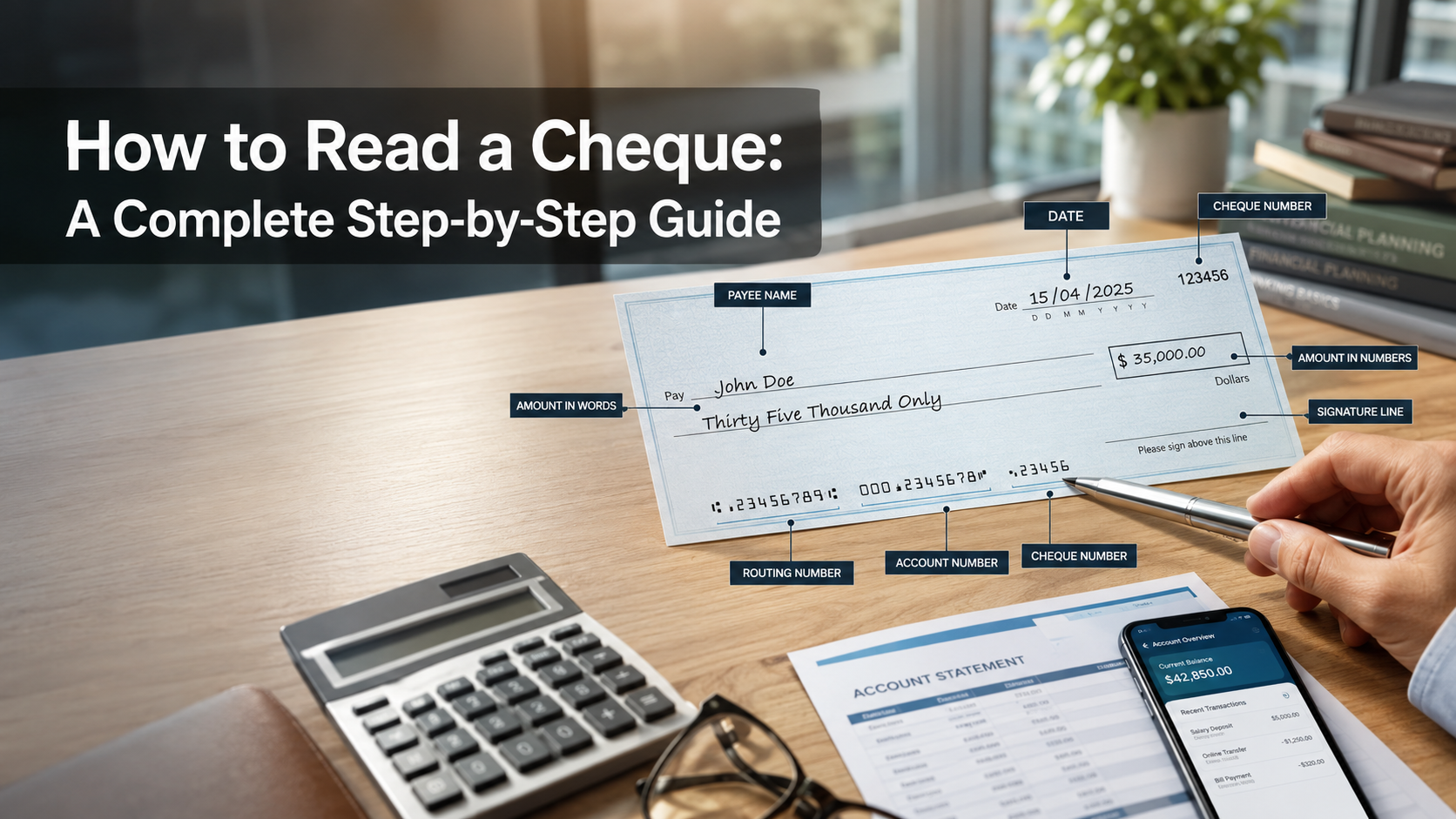

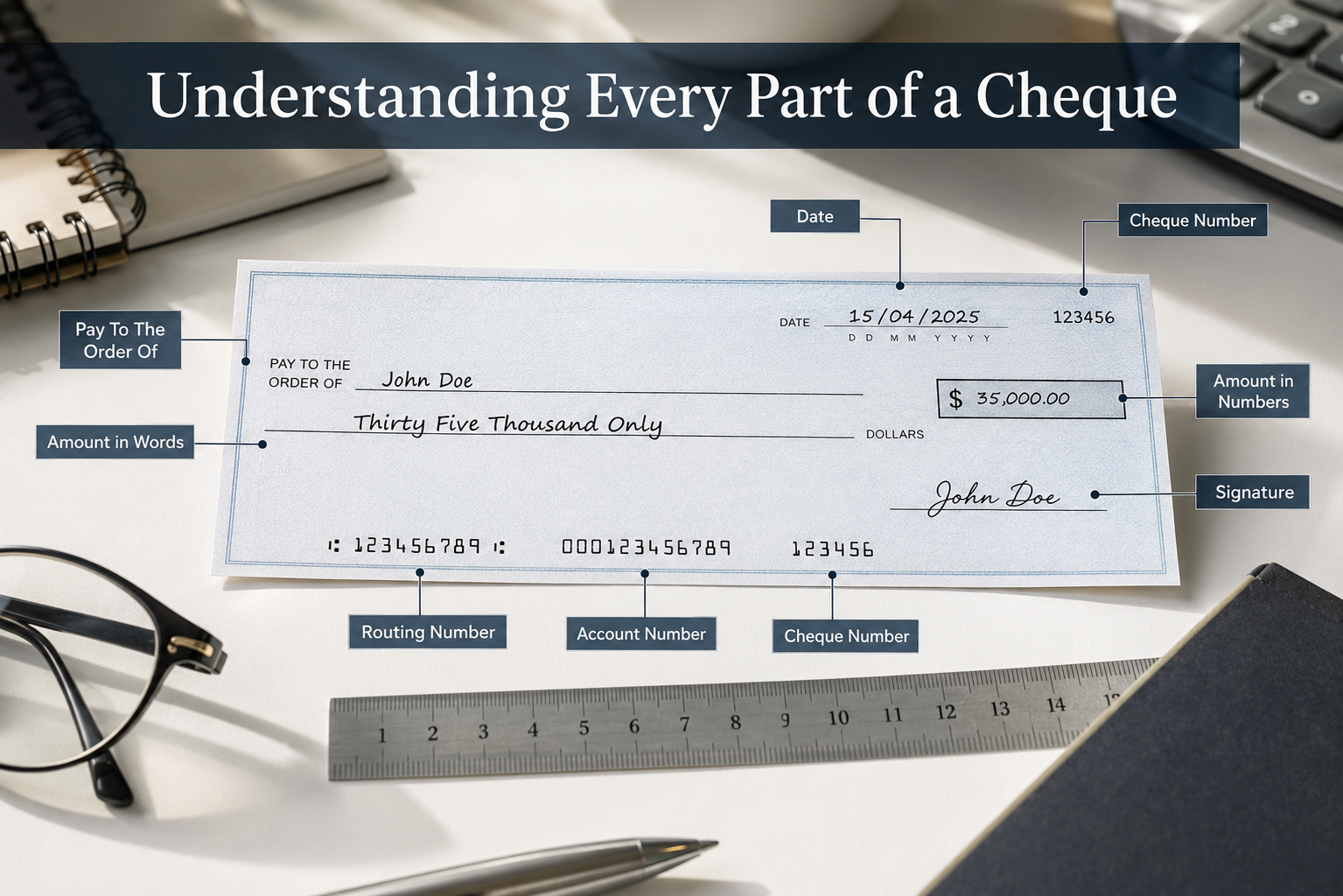

When you first look at a cheque, the amount of information printed on such a small piece of paper can feel overwhelming. However, every financial institution follows a strict template to keep processing simple. Each section serves a legal purpose to ensure the validity of the transaction. By breaking down the front layout into manageable parts, you can easily identify who is paying, who is receiving, and which bank is managing the exchange of funds.

Personal and Bank Information

In the top-left corner, you will find the account holder’s personal details. This includes the legal name and the registered mailing address. Directly opposite or just below this section, the printing displays the name of the bank or financial institution holding the funds. Having this information visible helps businesses verify the identity of the person writing the cheque. It also gives the recipient peace of mind knowing exactly which bank is backing the financial document being handed over to them.

The Essential Transaction Fields

The middle portion of the cheque contains the specific details required to execute the transaction:

-

The Date Line: Located in the top right, this dictates when the cheque becomes valid for cashing or depositing.

-

Pay to the Order of: This line specifies the exact individual or organization authorized to receive the funds.

-

The Amount Boxes: The cheque features two distinct areas for the payment amount. A small box displays the amount in numbers (e.g., $150.00), while a long line requires you to write the amount out in words.

Every field must be filled out completely to prevent fraud or processing rejections. If you leave the payee line blank, anyone can write their name in and cash the document. Similarly, writing an incorrect date can cause the bank to refuse the deposit altogether.

How to Read a Cheque: Deciphering the Bottom Numbers

The bottom edge of every cheque contains a string of uniquely stylized numbers. Banks use Magnetic Ink Character Recognition (MICR) technology to read this line automatically. Understanding this section is the core of mastering how to read a cheque. These numbers communicate directly with banking computers to transfer funds instantly.

The Transit Routing Number

The first nine digits on the left side represent the routing number. This code identifies the specific financial institution responsible for clearing the funds. Think of it as a postal code for your bank, directing the money to the correct corporate entity. Without this precise nine-digit sequence, clearing houses would not know where to send the transaction requests. It is a vital piece of data required for setting up automated payments or receiving electronic transfers from employers.

The Account Number

The middle set of numbers identifies your personal or business checking account. This sequence tells the bank exactly which vault or ledger to pull the money from once the routing number locates the correct institution. Every account holder has a unique sequence, ensuring that funds are never drawn from the wrong person. When providing banking details for external transfers, you will always copy this exact sequence alongside your routing code to establish a secure link.

The Cheque Number

Usually the shortest sequence on the bottom line, this matches the sequential number printed in the top-right corner. It helps you track individual payments and allows banks to flag duplicate transactions. Using this tracking code helps you maintain accurate record-keeping in your personal ledger. If a cheque goes missing or gets stolen, you can provide this specific number to your bank to issue a stop-payment order quickly.

Key Security Features and the Reverse Side

The back of a cheque is just as important as the front. It contains security measures and validation fields that ensure the funds reach the intended recipient safely. Many users completely ignore the back until they need to sign it, but understanding its layout helps protect against sophisticated counterfeiting methods.

The Endorsement Area

Flip the cheque over, and you will see a designated area that reads “Endorse Here.” The recipient must sign this line before depositing or cashing the cheque. Writing “For Deposit Only” along with an account number adds an extra layer of security, preventing anyone else from cashing it if it gets lost. This simple endorsement practice ensures that your funds remain safe even if the physical piece of paper drops out of your wallet on the way to the bank.

Tracking Security Guards

Modern cheques use advanced printing techniques to deter fraud. Look closely at the back for a “Security Screen” warning box. Many cheques feature microprinted text that looks like a solid line to the naked eye but reveals distinct words under magnification. These high-tech features prevent criminals from photocopying or altering the document. If any of these security patterns appear distorted or missing, a bank teller will immediately flag the cheque for manual fraud investigation.

Common Myths About Processing Cheques

Many consumers hold misconceptions about how paper payments function in today’s digital landscape. Clearing up these myths helps protect your financial health and prevents unexpected fees. As technology evolves, the laws governing physical transactions change as well, making old assumptions dangerous for your account balances.

Do Cheques Last Forever?

A common misconception is that a cheque remains valid indefinitely. In reality, banks consider cheques “stale-dated” after six months. While some institutions may still honor them, they have the legal right to refuse processing. If you find an old payroll or personal cheque tucked away in a drawer, it is always best to contact the issuer for a replacement rather than risking a returned document fee at your local branch.

The Speed of Digital Clearing

Many people assume paper cheques take weeks to clear. Thanks to electronic check conversion laws, banks scan images of cheques instantly. The funds often leave your account within 24 hours, meaning you should never write a cheque assuming you have a few days to deposit the cash. This rapid clearing cycle makes it imperative that you have the full amount available in your balance at the exact moment you hand the paper over.

Frequently Asked Questions

What do the numbers at the bottom of a cheque mean?

The numbers at the bottom of a cheque are written in a special magnetic ink and are divided into three distinct sections. The first nine digits represent the routing number, which identifies your specific bank. The second string of numbers is your unique account number, telling the bank where to pull the funds from. The final, shorter set of digits is the cheque number, which helps track individual transactions. Together, these numbers allow automated sorting machines to process payments accurately and quickly without manual data entry. It serves as the primary communication link between different banks.

This entire row is called the MICR line, which stands for Magnetic Ink Character Recognition. Banks use specialized sorting machines that read this magnetic ink even if someone has written over it or smudged the paper. Understanding this sequence allows you to quickly find the exact information you need when setting up online bills, linking external accounts, or authorizing one-time electronic payments over the phone.

Where is the routing number located on a cheque?

The routing number is always located at the bottom-left corner of a standard cheque. It consists of exactly nine digits and is flanked by specific symbols known as MICR characters. This number functions as an address for your financial institution. When a business or bank scans your cheque, this number instantly tells its computer system which bank holds your checking account. It is the first set of numbers you read from left to right on the bottom line. Finding this number is essential whenever you need to set up recurring automated bill payments online.

In some cases, large national banks use different routing numbers for different states or regions. Therefore, always check the bottom-left corner of your own cheque to verify the correct number. This method is more accurate than relying on a family member’s or coworker’s account information.

How do you read a cheque for direct deposit?

To set up a direct deposit, you need to read the routing number and account number from the bottom of your cheque. Look at the bottom-left corner to find the nine-digit routing number and write it down. Next, look at the middle sequence of numbers to locate your specific account number. Ignore the cheque number entirely for this process. Employers use these two codes to route your paycheck directly into your checking account electronically, eliminating the need for paper delivery. It provides a secure, completely paperless path for your recurring income streams.

When you look at the sequence, you might see small symbols that look like brackets separating the numbers. Do not include these symbols when filling out your direct deposit enrollment form; only copy the numerical digits themselves. If your check does not clearly separate the account number from the check number at the bottom, you can cross-reference it with your monthly bank statement to ensure absolute accuracy.

What is the difference between the routing number and account number?

The routing number identifies the financial institution itself, acting like an institutional zip code. The account number identifies your specific, individual account within that financial institution. Multiple customers at the same bank will share the exact same routing number, but no two customers will ever share the same account number. When reading a cheque, the routing number appears first on the left, while the account number typically follows it in the middle string of digits. Knowing the difference ensures you fill out financial enrollment documents without mixing up critical identification codes.

If you accidentally swap these two numbers on an electronic form, your transaction will fail entirely. The automated clearing house network will try to look for a bank using your account number, fail to find it, and reject the payment request immediately. This error can result in late fees from billing companies or significant delays in receiving your hard-earned payroll deposits.

Why is the amount written twice on a cheque?

The amount is written twice on a cheque to prevent fraud and minimize administrative errors. First, the numerical box gives the bank teller a quick reference for the value. Meanwhile, the written line spells out the amount in words for legal validation. If, however, a discrepancy occurs between the numbers in the box and the written words, legal guidelines state that the written words always take precedence as the official legal amount of the cheque. As a result, this legal rule protects consumers from malicious alterations because words are much harder to rewrite or modify than simple numbers.

For example, a scammer could easily add a zero to the end of the numbers box, turning a fifty-dollar cheque into a five-hundred-dollar cheque. However, changing the handwritten words “Fifty and 00/100” to match that fraudulent addition requires completely rewriting the sentence. Consequently, the document is far more likely to be flagged as tampered with. Therefore, always write out the words clearly and draw a straight line to fill any remaining blank space on that line.

Conclusion

Mastering how to read a cheque gives you greater control over your banking transactions. Once you understand how to read a cheque, you can identify routing codes, account numbers, and security features with confidence. This knowledge helps you avoid processing delays and reduces the risk of banking fraud. Always double-check your written amounts before handing over a cheque. Also, confirm that all numbers are correct. This simple habit keeps your personal finances running smoothly and securely. It also bridges the gap between traditional cheque security and modern electronic processing systems.

Although digital banking continues to grow, paper cheques remain a reliable option for large payments. These include home down payments, vehicle purchases, and business contracts. Learning how to read a cheque removes uncertainty during these important transactions. You no longer have to guess which number belongs on an online payment form. Nor do you need to worry about a teller rejecting your deposit. Taking time to master how to read a cheque builds long-term confidence. It also helps protect your financial well-being for years to come.